{kind=link}

Table of Contents

Did you know that in 2019, tax revenues in the European Union (EU-27) averaged 40.1% of GDP? This shows how crucial optimal taxation is. It has changed a lot with insights from behavioral economics. Welcome to our guide on optimal taxation with behavioral agents. We’ll look at how taxpayers’ biases can help make better tax policies.

We’ll explore the basics and evidence of optimal taxation, behavioral economics, and public finance. We’ll cover the Ramsey, Pigou, and Mirrlees models, and new ideas like agent-based modeling and nudge theory. These ideas are key for fiscal policy, incentive design, tax incidence, and welfare analysis.

If you’re into policy, research, or just curious about how humans and taxes interact, this article is for you. Let’s start an interesting journey to learn about optimal taxation with behavioral agents.

Key Takeaways

- Optimal taxation with behavioral agents looks at how biases affect tax policy.

- Using behavioral insights can lead to lower tax rates, especially for low incomes. It might even justify work subsidies like the Earned Income Tax Credit.

- Present bias in work choices is important for optimal taxation. Studies show it affects how many hours people work.

- Flexible work options, becoming more common, might be affected by present bias in labor supply decisions.

- To have an optimal tax system, we need to balance making money and reducing tax distortions. We must consider both traditional and behavioral factors.

Introduction to Optimal Taxation with Behavioral Agents

Taxation can seem complex, but knowing the basics is key for good policies. We’ll look at the background of traditional tax models and why we need to add behavioral insights.

Background on Traditional Optimal Taxation

Classic tax theories, like Ramsey, Pigou, and Mirrlees, are the foundation of tax policy. These ideas, from economists like Frank Ramsey and James Mirrlees, help us understand the best tax structures.

Need for Incorporating Behavioral Insights

But, these models assume people make rational choices, which isn’t always true. People have biases and heuristics that affect how they react to taxes. Adding these behavioral aspects to tax policies is now a major focus for experts in public economics.

“The growing recognition that individuals often do not behave in accordance with the assumptions of traditional economic models has highlighted the importance of incorporating behavioral factors into the design of optimal tax policies.”

By understanding biases like misperceptions and present bias, we can make better tax policies. This section will explore how behavioral economics helps in making taxes more effective and beneficial for everyone.

Behavioral Biases and Their Impact on Taxation

Behavioral biases and decision-making heuristics greatly affect how people react to taxes. The field of behavioral public finance has shown how these quirks change the usual ideas about the best tax systems.

Loss aversion is a big one. People feel the pain of losing more than the joy of gaining. This makes them choose tax systems that avoid big losses, like withholding taxes, even if they’re not the best. Framing effects also matter, as how tax info is presented can sway decisions.

- Present bias makes people less interested in long-term tax benefits.

- Wrong ideas about tax rates and their effects can mess up tax policies.

- Mental accounting, treating money differently based on its source, can lead to bad tax responses.

These biases mean we might need to rethink traditional tax models. Adding these insights helps us understand tax policy better. It also improves welfare analysis and tax policy.

“The study highlights modifications to canonical optimal tax formulas when dealing with behavioral agents.”

By recognizing behavioral biases and decision-making heuristics, policymakers can create better tax systems. These systems will better match human behavior and improve welfare.

Revisiting the Three Pillars of Optimal Taxation

The three main pillars of optimal taxation are Ramsey, Pigou, and Mirrlees. But, when we add behavioral agents, things get interesting. We see how these classic ideas change with behavioral biases and heuristics.

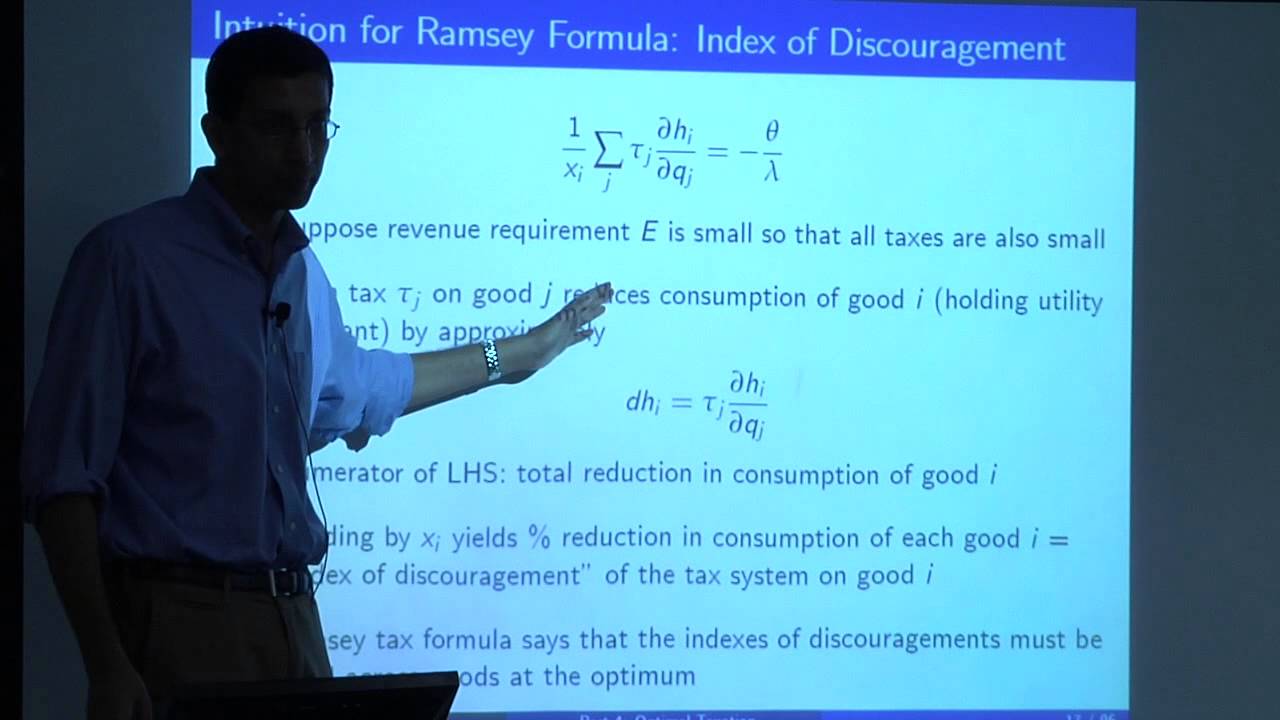

Ramsey Taxation with Behavioral Agents

The Ramsey model focuses on taxes for making money. But, with behavioral agents, we need to rethink it. We must adjust the tax formulas to deal with biases in consumer choices.

Things like misperceptions and mental accounting play big roles. They affect how much people buy and sell, changing the best tax rates.

Pigou Taxation with Behavioral Agents

Pigou taxation is known for fixing market problems with taxes. But, with behavioral agents, it gets more complex. Biases and heuristics change what taxes are needed to fix issues.

Studies show how inattention and limited choices affect Pigouvian taxation. This leads to new economic ideas.

“The key is to recognize that behavioral biases can significantly influence the economic outcomes and, therefore, the optimal tax policies. By incorporating these insights, we can design more effective and welfare-enhancing taxation systems.”

Behavioral agents and optimal taxation are a fascinating area to study. As we learn more about how behavior affects economics, we can make better tax policies.

Mirrlees Income Taxation with Behavioral Agents

The traditional Mirrlees framework for optimal nonlinear income taxation has been key in optimal taxation theory. But, as we explore behavioral economics, we see the need to update the Mirrlees model. This is to reflect the unique traits of behavioral agents.

Recent studies have looked into how Mirrlees taxation and nonlinear income taxation should be shaped for behavioral agents and optimal taxation. These findings offer crucial advice for policymakers dealing with the challenges of optimal taxation and behavioral biases.

- Limited attention to taxes: The study shows that optimal taxes need adjustments for agents with limited tax focus. This affects the structure of the optimal income tax schedule.

- Heterogeneous attention: With agents having different levels of attention, tax tools can cause misallocation. This is a big challenge for optimal taxation.

- Internalities and redistribution: The study points out the balance between fixing internalities with taxes and keeping effective redistribution. It suggests using nudges to target internalities without harming distribution.

This research builds on Ramsey, Pigou, and Mirrlees’ work. It gives a detailed look at how to include behavioral biases in designing optimal income taxes. As policymakers face the complexities of today’s tax systems, this research offers important insights for optimal taxation with behavioral agents.

“The paper generalizes optimal tax formulas derived by Diamond (1975), Sandmo (1975), and Saez (2001), providing a comprehensive framework for designing optimal taxes in the presence of behavioral biases.”

optimal taxation with behavioral agents

In the world of public finance, adding behavioral insights to the traditional optimal taxation framework is key. By understanding cognitive biases and heuristics, we see how people react to taxes better.

The behavioral approach to optimal taxation questions the old ideas of rationality and full information. It looks at how biases, like misperceptions and mental accounting, shape tax policies.

Researchers have looked into how behavioral biases affect the core of optimal taxation – Ramsey, Pigou, and Mirrlees. They’ve found new ways to make optimal taxation work for behavioral agents in public finance and fiscal policy.

The agent-based modeling method is a big help here. It lets researchers see how behavioral agents and taxes interact. This way, policymakers can understand how biases affect tax plans.

“The inclusion of behavioral insights in optimal taxation frameworks has opened up new ways to study fiscal policy in the real world.”

The study of optimal taxation with behavioral agents is growing. It’s giving us insights that can lead to better and fairer public finance policies. This will help improve the lives of citizens and the economy.

Incorporating Nudges into Optimal Taxation

Optimal taxation is a complex challenge for policymakers. A new area of research combines nudge theory with optimal taxation. This shows how behavioral nudges can make tax policies more effective and improve society.

Nudge Theory and Applications

Nudge theory suggests that small changes can greatly affect our behavior. These behavioral nudges use our biases to guide us towards better choices. In taxes, nudges can be defaults, how we frame things, or giving us key information.

Optimal Taxation and Nudges

Combining nudge theory with optimal taxation is a new area. Researchers are finding ways to use taxes and nudges together. This aims to boost savings, encourage healthy habits, or reduce losses from biases.

This research could change how we make tax policy and analyze welfare. As we learn more about behavioral nudges and optimal taxation, we’ll see smarter policy designs. These will better match the complexities of human behavior.

“The integration of nudge theory and optimal taxation has opened up a new frontier in policy design.”

Empirical Evidence on Behavioral Biases and Taxation

Behavioral economics is growing, showing how biases affect taxes. Researchers have found many insights that question old ideas about how we make tax decisions.

Misperceptions about taxes can change the best tax rate. For example, if people think taxes are 25% more or less than they really are, the best tax rate changes a lot. For people who are different, the best tax rate is 7.29%. But for people who are the same, it’s 20.3%, which is 2.78 times higher.

The salience of taxes also matters a lot. If everyone knows exactly how much taxes are, the best tax rate is just 1.27%. This shows how important it is to think about biases when making tax rules.

“The more powerful the nudge is for high-internality agents, the more optimal policy relies on the nudge rather than the tax.”

Studies also look at how nudges and taxes work together. They found that nudges and taxes can be used together in the best policy. This is true when the social value of money and the power of nudges go in opposite directions.

This research shows that tax policies need to consider how biases affect us. By understanding these biases, tax policies can be made better. This helps achieve the goals of tax policies.

Welfare Analysis with Behavioral Agents

Optimal taxation faces challenges due to behavioral biases in decision-making. This section explores how these biases affect welfare analysis with behavioral agents.

The research shows that biases like misperceptions and mental accounting change traditional tax policy views. It finds that, under certain conditions, taxes can be simple with all rates equal. This challenges the idea that taxes should be simple for efficiency.

The study also notes that bounded rationality can lead to uniform tax rates. But, behavioral biases can make classical results on supply elasticities and production efficiency fail.

“The misperception distribution among heterogeneous agents is a 2-point distribution with specific properties such as mh = 1 with probability p, and a with probability 1 – p.”

The research shows that the optimal tax ratio changes with agent behavior heterogeneity. This highlights the need to consider behavioral biases in welfare analysis and optimal taxation policy design.

In summary, this section discusses the challenges in welfare analysis with behavioral agents in optimal taxation and decision theory. It stresses the importance of understanding how biases alter policy evaluation and design.

Policy Implications and Challenges

Optimal taxation with behavioral agents brings up many policy issues and challenges. Policymakers face a complex world where old ideas about how people behave are no longer true. Behavioral economics shows us that people don’t always act rationally.

One big issue is figuring out how to measure and deal with behavioral biases in taxes. Loss aversion, mental accounting, and hyperbolic discounting greatly affect how people react to taxes. To make the best tax systems, we need to understand these biases well.

- Dealing with different behaviors: People behave in many ways, and making one tax policy for everyone is hard. We might need to make policies that fit each person’s behavior better.

- Meeting many goals at once: With behavioral agents, tax policies get even more complicated. Policymakers have to balance making money, helping the poor, and changing behavior. Finding the right mix is very tricky.

- Using nudges and choice architecture: Small changes, like nudges and choice architecture, can really change how people make tax decisions. Adding these to tax policies can make them work better.

The challenges of optimal taxation with behavioral agents are big and need teamwork from policymakers, economists, and behavioral scientists. By tackling these issues, we can make tax systems that work well and match how people really behave.

“You never let a serious crisis go to waste. And what I mean by that it’s an opportunity to do things you think you could not do before.” – Rahm Emanuel

As we face these policy implications and challenges, staying flexible and open to new ideas is key. By using the latest from behavioral economics, we can aim for tax policy designs that really meet the needs of our behavioral agents.

Emerging Research Directions

The field of optimal taxation with behavioral agents is growing fast. Researchers are looking into new ways to study it. They want to understand how our minds affect tax policies and how these policies impact us and society.

Another area of study is dynamic taxation with bounded rationality. This means looking at how taxes change over time because of our limited thinking. It helps us see how tax schemes might need to adjust as our behaviors and decisions change.

Experts are also studying how behavioral biases work with other policy tools, like nudges. They’re finding out how these tools can work together to make tax systems better and more fair.

Finally, combining behavioral economics with public finance and decision theory is a big area of research. This mix of ideas is helping us see new ways to think about taxes, behavioral economics, and public finance.

- Integrating behavioral models with agent-based simulations to capture the dynamic interplay between cognitive biases and tax policy

- Analyzing dynamic taxation with bounded rationality to account for changing behavioral patterns over time

- Exploring the interplay between behavioral biases and other policy instruments, such as nudges, to design effective and welfare-enhancing tax systems

- Integrating behavioral economics principles with theories of public finance and decision theory to uncover novel perspectives on optimal taxation

“The future of optimal taxation with behavioral agents lies in the seamless integration of theoretical insights, empirical evidence, and innovative modeling techniques. As we continue to push the boundaries of our understanding, we can unlock transformative solutions for more equitable and efficient tax systems.”

Conclusion

As we wrap up our look at optimal taxation with behavioral agents, it’s clear that using insights from behavioral economics can make tax policies better. By understanding how people’s biases and decision-making affect their tax responses, we can create more effective tax systems. These systems will better match how people actually behave.

In this article, we’ve seen how behavioral biases affect the three main parts of optimal taxation. We’ve also talked about how nudges can influence tax decisions and why welfare analysis is key. The evidence shows that tax attitudes and behaviors are complex. This means policymakers need to think about these factors when making tax policies.

The future of optimal taxation with behavioral agents is bright. As we learn more about how people handle tax information and make decisions, we can improve tax policies. These policies will be more effective and fair for everyone, including businesses and individuals.

For more on how to plan for retirement as a business owner, check out this article.